NtInsight® for OpRisk

Simulations of patterns to model operational risk in real life.

NtInsight for OpRisk is an operational risk management software designed to cater to the requirements of financial institutions that have selected the advanced measurement approach (AMA) to calculate their required capital for operational risk.

Key Differentiators

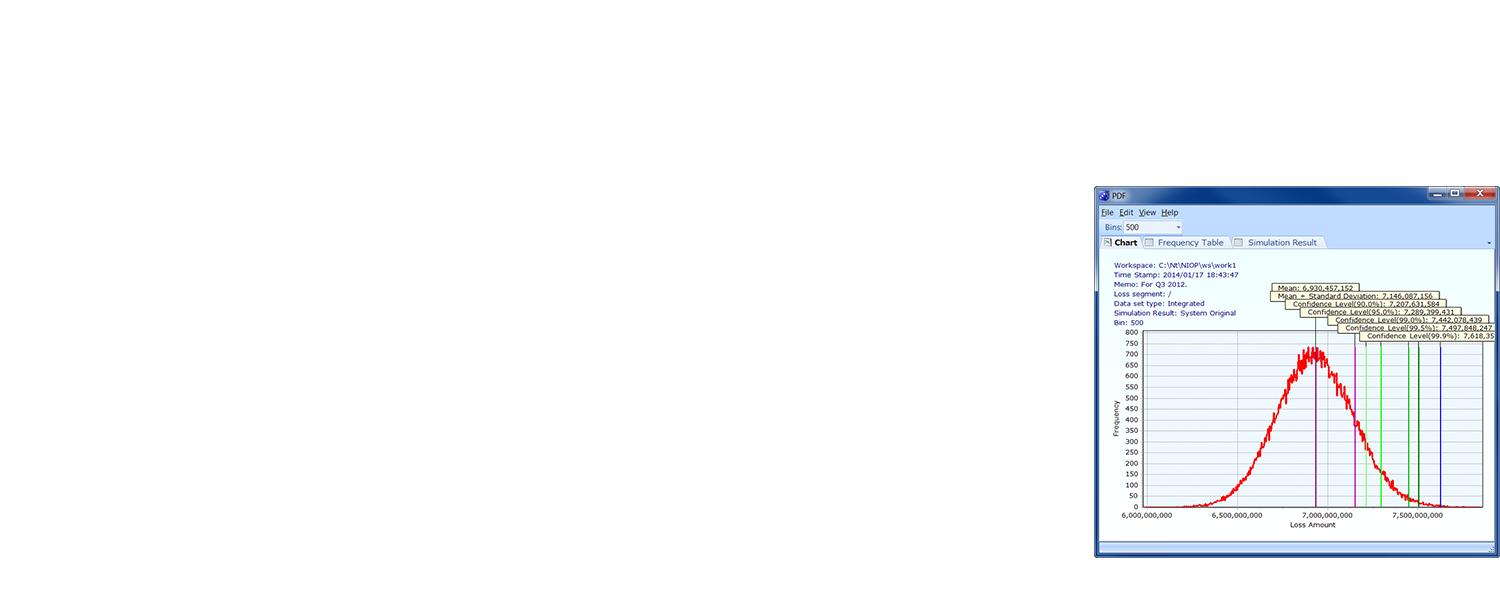

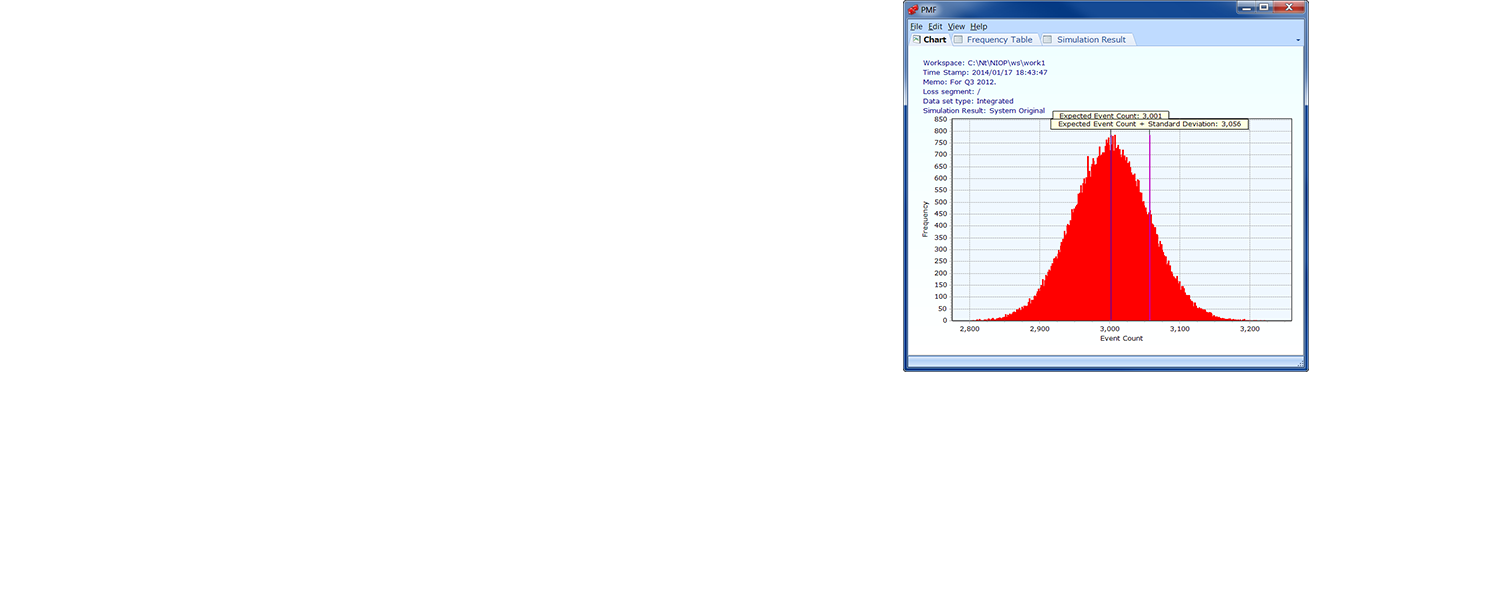

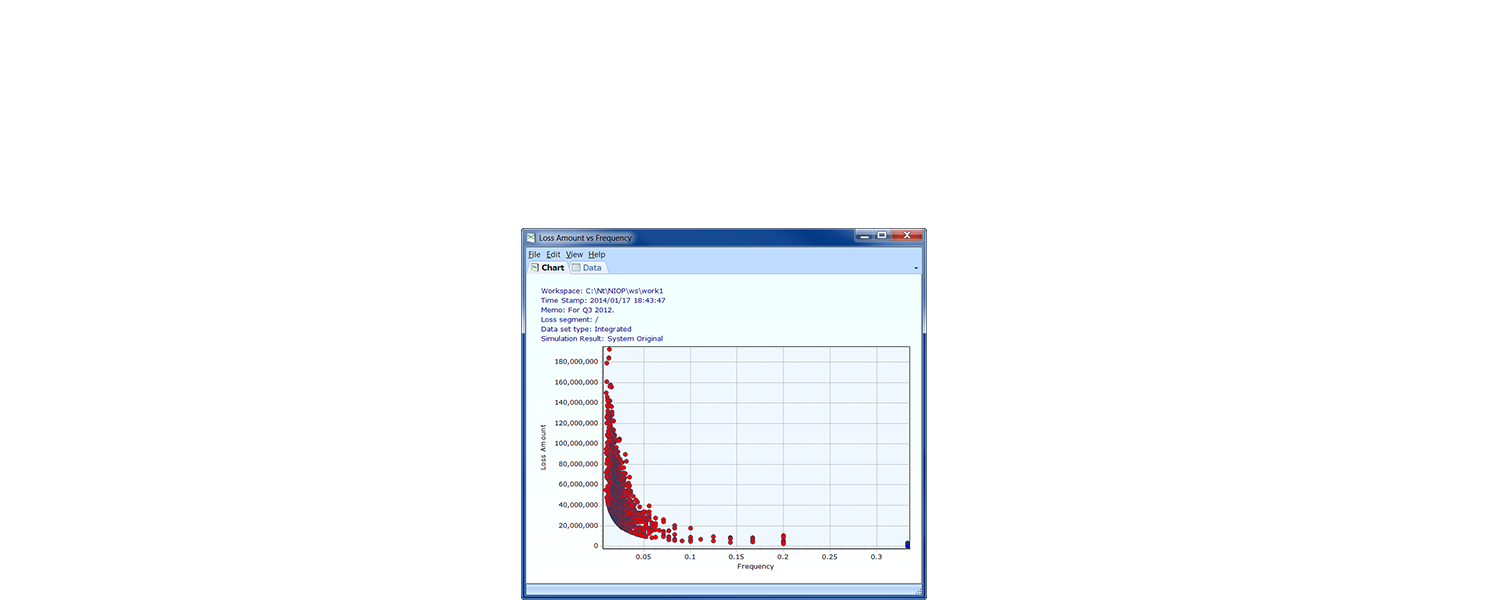

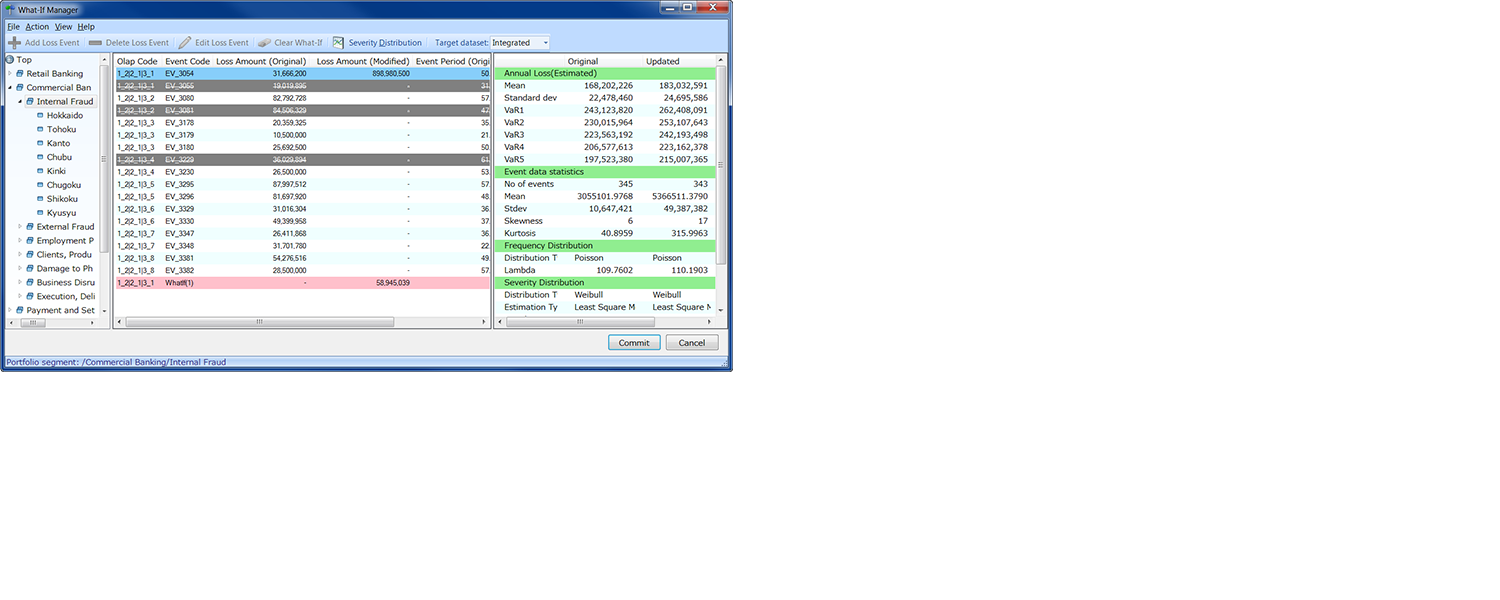

NtInsight for OpRisk accurately calculates a financial institution’s required capital through its sophisticated Monte Carlo simulation engine. It is the only operational risk management software that can generate the various simulation patterns supported by Loss Distribution Approach.

Sophisticated Modeling Technique

Compute economic capital using loss distribution approach (LDA), an AMA approach recognized by the Basel II framework and is the most sophisticated AMA approach available today. LDA supports both parametric and non-parametric simulation functions.

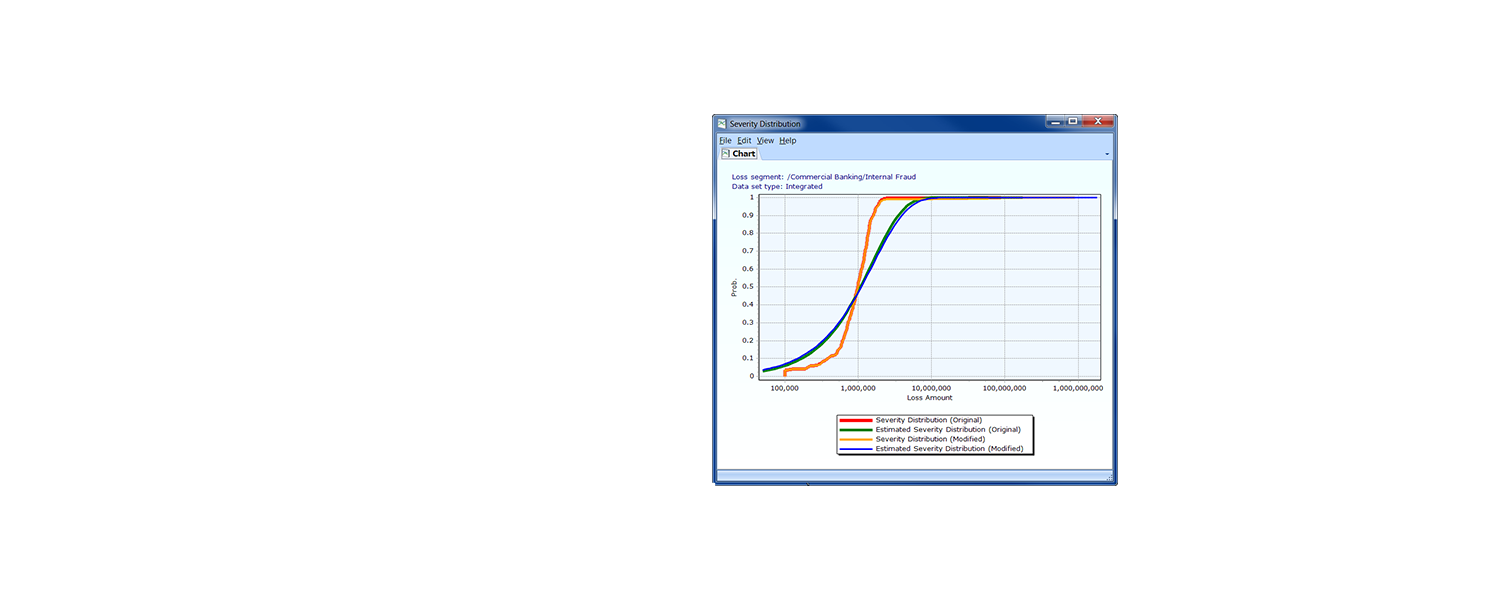

Wide Selection of Distribution Functions

NtInsight for OpRisk provides an interpolation algorithm to stabilize simulation results in non-parametric simulation. It also supports various frequency distribution and severity distribution functions for parametric simulation such as:

- Poisson Distribution

- Weibull Distribution

- Log-Normal Distribution

- Gamma Distribution

- Pareto Distribution

Multidimensional Risk Analysis

Normally, operational risk is calculated according to a matrix of business lines and operational risk types. NtInsight for OpRisk gives you the flexibility to add different perspectives and depths (such as business department, department divisions, and sections) in your operational risk analysis.

Regulatory Capital Requirement Support

NtInsight calculates the minimum capital requirements stipulated in Basel II/III.