AccuracyCalculate without simplification or approximation

TransparencyUncover black box and track at a granular level

FlexibilityLocalize to cater to unique needs

ElasticityScale the functionalities to fit with the right solution

SpeedLeverage HPC to optimize speed-accuracy

NtSaaS®

NtSaaS is a next-generation risk management platform. Solutions derived from the best of our knowledge and product development are now available in Software as a Service.

Find your solutionsNtInsight®

NtInsight is a suite of risk management software covering Asset Liability Management (ALM), market risk, credit risk, and operational risk. It has been used by world’s top-tier banks since 1998.

Find your solutionsNtEdge®

NtEdge is our latest product series designed with flexibility to adapt to user’s existing environment and requirement.

Find your solutionsSolutions

Financial risk management software designed to meet present and future regulatory requirements.Basel III & IRRBB

Enhance our solutions’ features in accordance with the latest banking regulation.

ORSA & Solvency II

Forecast financial statements on a Market Consistent Valuation (MCV) basis.

IFRS

Implement IFRS 9 with ready-to-use framework for Expected Credit Loss (ECL) model components.

Funding & Investment Planning

Simulate with flexibility along a time axis for daily funding operations, accounts settlement, and investment planning.

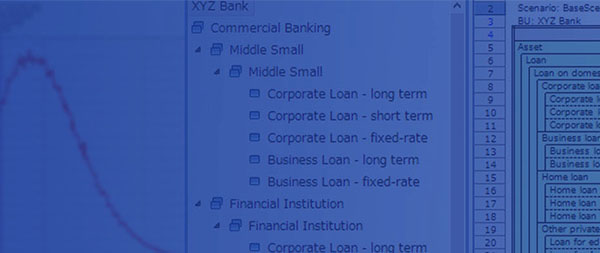

Online Analytical Processing

Analyze the entire portfolio’s risk profile interactively from multiple perspectives such as business unit, region, industry, or other pre-defined segments.

Fat-Tail Risk Awareness

Model and include extreme or black swan events in scenario analysis or stress testing with implementation of Johnson’s SU-normal distribution.

"Every software is programmed, but some softwares are programmed well."

Our Mission

To become a trusted partner with financial institutions in Financial Risk Management and help them to protect the world.

About UsWhy choose Us

We are a leading risk management software company from Japan and counts the top-tier banks and insurance firms as its long-term partners.

Contact UsJoin Us

Numerical Technologies is driven by a select group of professionals. We expect only the best from our team; in return, we offer competitive salaries, attractive benefits and a challenging but relaxed working environment.

Read More